Foreign and domestic companies bringing genuinely new products, processes, or technologies into the Philippines can apply for Pioneering Status with the Board of Investments (BOI). It's one of the most valuable classifications available under Philippine investment law.

Projects that qualify get several benefits, including the longest Income Tax Holiday available under Philippine investment law. Additionally, there are duty exemptions on imported capital equipment and several other fiscal and non-fiscal benefits.

This guide walks through how Pioneering Status works today, who qualifies, and how to apply.

Understanding a Pioneer Project

Pioneering Status is a classification granted by the BOI to projects that introduce something genuinely new to the Philippine market. This can be a product not yet produced commercially in the country, a process or technology not currently used domestically, or a service that doesn't have a meaningful local equivalent.

Pioneer projects qualify for the longest available Income Tax Holiday (six years versus four for non-pioneer projects), plus eligibility for incentive packages under the Strategic Investment Priority Plan (SIPP) tier system.

It's important to know that this is not a separate application. It's an assessment outcome during BOI registration where the agency evaluates whether your project meets the pioneer criteria under the Omnibus Investments Code (Executive Order 226).

A project may qualify as pioneer if it meets one of these conditions:

- Engages in commercial production of goods, products, or raw materials not yet produced in the Philippines on a commercial scale

- Uses a design, formula, scheme, method, process, or production system that is new and untried in the Philippines

- Produces non-conventional fuels or uses non-conventional energy sources in its production

- Engages in agricultural, forestry, or mining activities considered highly essential to national food self-sufficiency or specific national programs

For foreign investors, the pioneer route is one of three qualifying paths to BOI registration. Wholly foreign-owned enterprises can register if they either:

- undertake a pioneer project,

- export at least 70% of their production

- locate in a Less Developed Area designated by the BOI.

How Pioneer Projects Fit Within the SIPP Framework

The Strategic Investment Priority Plan is the master document identifying activities eligible for fiscal incentives under CREATE MORE. The current 2022 SIPP is in force, with a successor plan in development since early 2025.

The SIPP categorizes activities into three tiers:

- Tier I includes activities the government considers foundational, such as healthcare and disaster risk reduction, environment and climate-change projects, agriculture and fisheries, mass housing, infrastructure and logistics, and certain manufacturing.

- Tier II covers activities supporting industrial competitiveness, including more advanced manufacturing, supply chain integration, and value-added processing.

- Tier III covers innovation and technology-driven activities, including research and development, IT-BPM, and frontier technologies.

A project can be classified as pioneer status within any tier if it meets the pioneer criteria.

The tier determines the length and scope of incentives available; pioneer classification affects which incentives within that tier package the project qualifies for.

Higher tiers generally come with longer enhanced deduction periods and more generous customs and VAT treatments.

Incentives Available to Pioneer Projects

Under CREATE MORE, the incentive package depends on whether your project is classified as a Registered Export Enterprise (REE) or a Registered Domestic Market Enterprise (DME).

For Registered Export Enterprises

Export-oriented projects (exporting at least 70% of production) can choose between three options:

- ITH of 4 to 7 years, followed by either Special Corporate Income Tax (SCIT) or Enhanced Deductions Regime (EDR) for 10 years

- SCIT immediately at the start of commercial operations, for a maximum of 14 to 17 years

- EDR immediately at the start of commercial operations, for a maximum of 14 to 17 years

Pioneer projects typically qualify for the longer end of the ITH range (six years), with the specific duration depending on location and SIPP tier.

For Registered Domestic Market Enterprises

Domestic market projects have two options:

- ITH of 4 to 7 years, followed by EDR for 10 years (extended to 20 years for projects approved at the IPA level under specific conditions)

- EDR immediately at the start of commercial operations, for a maximum of 14 to 17 years (extended to 24 to 27 years in certain cases)

How ITH, SCIT, and EDR Work

- Income Tax Holiday (ITH) is full exemption from corporate income tax during the holiday period. For pioneer projects, the standard duration is six years (versus four for non-pioneer projects), with longer periods available in Less Developed Areas.

- Special Corporate Income Tax (SCIT) is a 5% tax on gross income earned, in lieu of all national and local taxes. It's primarily used by export enterprises seeking predictable, simplified tax treatment.

- Enhanced Deductions Regime (EDR) lets you deduct more than the actual cost of certain expenses, including additional depreciation (10% for buildings, 20% for machinery), 100% additional deduction on power expenses (increased from 50% under CREATE MORE), 50% additional deduction on labor, and a 50% additional deduction on expenses for trade fairs and export promotion (available until 2034).

The incentive package you choose is irrevocable for the entire entitlement period, so the upfront analysis is important.

Export-oriented manufacturers often favor SCIT for its simplicity. On the other hand, domestic-focused enterprises and businesses with significant capital expenditures usually prefer EDR for the larger deductions.

Customs and VAT Benefits

Pioneer projects also receive:

- Duty exemption on imported capital equipment, raw materials, spare parts, and accessories used in the registered project

- VAT exemption on importation and VAT zero-rating on local purchases for export enterprises

- Optional 2% RBE Local Tax during ITH and EDR periods, in lieu of all local taxes (not applicable under SCIT)

Who Can Apply for Pioneering Status

Pioneering Status is available to both domestic and foreign-owned enterprises, with some structural differences in eligibility:

- Wholly Filipino-owned enterprises can register for BOI incentives if engaged in any activity listed in the SIPP, regardless of whether the project is pioneer or non-pioneer

- Wholly foreign-owned enterprises must either undertake a pioneer project, export 70% or more of their production, or locate in a designated Less Developed Area. Unless fully export-oriented, they're also required to transition to 60% Filipino ownership within 30 years of registration

The pioneer route is particularly relevant for foreign investors entering Philippine markets with technology, processes, or products that don't yet exist locally at scale.

The determination of eligibility and communication with the governmental institutions can be lengthy and need extra attention.

However, Emerhub’s consultants can ease your burden and handle the BOI and PEZA registrations on your behalf.

Contact us via philippines@emerhub.com to start now.

Learn more about the ways to maximize the tax incentives in the Philippines.

The Application Process

The application flows through the BOI for projects with investment capital up to USD 259 million (approximately PHP 15 billion). Above that threshold, applications are routed through the Fiscal Incentives Review Board (FIRB) for final approval.

Step 1: Incorporate Your Philippine Entity

Pioneer status applications require a registered Philippine business. For foreign investors, this typically means a domestic corporation, branch office, or representative office, depending on the activity.

The corporate structure must be in place before the BOI application can proceed.

Step 2: Prepare the Application Package

The standard documentation includes:

- Letter of Intent addressed to the BOI

- Comprehensive project study covering technical, financial, and economic feasibility

- Description of the pioneer aspects (new technology, process, or product)

- Market analysis covering local and export markets

- Projected investments, employment, and economic contribution

- Corporate documents (SEC registration, Articles of Incorporation, By-Laws, financial statements)

- Technical proof of innovation, including patents, licensing agreements, or technical specifications where applicable

The strength of the application hinges on demonstrating genuine novelty. Generic claims of "advanced technology" without specifics typically fail at evaluation. Concrete documentation of what's new about the project (compared to existing Philippine operations) carries the application.

Step 3: Submit to BOI

Applications are filed through BOI's electronic and physical channels. Under EO 226, an application is deemed approved if the BOI Board doesn't act on it within 20 working days of acceptance, subject to terms and conditions. In practice, complex pioneer applications take longer due to clarification requests, additional documentation requirements, and technical assessments.

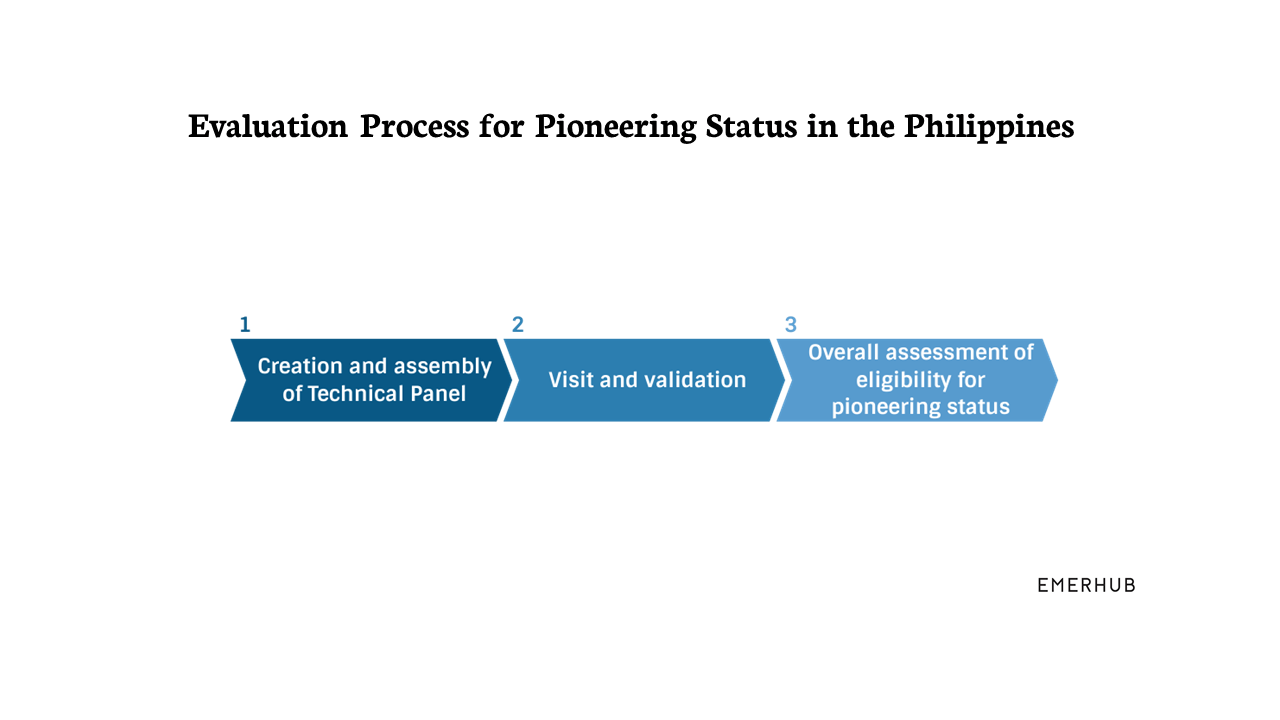

Step 4: Evaluation and Site Assessment

The BOI evaluates applications based on three primary factors: innovation level, economic contribution (employment, exports, value addition), and alignment with SIPP priorities.

The second stage of evaluation is the visit and validation during which the Technical Panel visits the company and evaluates whether your project qualifies for pioneering status in the Philippines.

This is especially common for projects involving physical manufacturing or specialized facilities.

Step 5: Certificate of Registration

Once approved, the BOI issues a Certificate of Registration specifying:

- The SIPP tier and pioneer classification (if granted)

- ITH duration and start date

- Available SCIT or EDR options and their terms

- Applicable non-fiscal incentives, including employment of foreign nationals and simplified customs procedures

- Ongoing compliance and reporting requirements

Total processing time from initial submission to Certificate issuance typically runs 3 to 6 months, depending on application complexity and how quickly clarifications and supplementary documents are provided.

How Emerhub Can Help

Emerhub's Philippines team handles the full process from incorporation through BOI registration and Pioneering Status application.

That typically means setting up the Philippine corporation with the right structure for incentive eligibility, preparing the project documentation that demonstrates pioneer characteristics, coordinating directly with the BOI throughout evaluation, and advising on whether to elect SCIT or EDR after the ITH period ends.

If you're already operating in the Philippines and considering expansion or a new project line that might qualify as pioneer, we can help assess whether the project meets the criteria before you invest in the full application.

Get in touch with our team to discuss your project and what the application would look like for your situation.

Need help with company registration in the Philippines? Have a look at our complete guide on how to register a corporation in the Philippines, too.

Frequently asked questions

Can existing companies apply for Pioneering Status, or only new businesses?

Both can apply, but the project under review must be new and meet the pioneer criteria. An existing company can apply for Pioneering Status on a new product line, a new technology, or a substantially innovative expansion. The pioneer status attaches to the project, not to the company overall.

Can a company hold multiple pioneer projects?

Each project is evaluated on its individual merits and gets its own Certificate of Registration with its own incentive period. Companies with multiple distinct pioneer projects need to maintain separate accounting for each registered activity, since the incentives apply to the specific project's income rather than to the company's overall earnings.

What's the difference between SCIT and EDR?

SCIT is a flat 5% tax on gross income, replacing all other national and local taxes. EDR allows enhanced deductions against your normal corporate income tax. While SCIT is simpler and more predictable; EDR can produce a lower effective tax rate for businesses with significant deductible expenses (large capital expenditures, high power consumption, substantial labor costs). The right choice depends on your cost structure and tax planning preferences. Once elected, the choice is irrevocable for the full duration.